When the COVID-19 pandemic hit Ho Chi Minh City, last year, the government ordered the closure of all businesses with the exception being for that of essential commodities. Mass gatherings had to be limited, people were not allowed venture outdoors unless necessary, and all aspects of social life were seriously impacted.

Instead of being dissolved, businesses had the option of a business suspension for a specified length of time, after which it would be able to resume normal operations.

1. Business suspension defined

A business suspension is when an enterprise suspends its business operations for a certain period of time due to various reasons such as financial difficulties, labor, etc., and is temporarily unable to continue business operations, and needs time to rearrange work, reassess finances, and perhaps restructure their operations.

2. Procedures for business suspension

The enterprise must submit written notification of the time and duration of the suspension to the business registration agency at least three (3) days prior to the planned date of suspension.

The notification must be enclosed with the resolution or decision and a copy of the minutes of the meeting of the Board of Members (for multi-member limited liability company) or partnership, of the Board of Directors (for joint-stock company), or the resolution or decision of the owner on business suspension for a single-member limited liability company.

3. Duration

While there is now limit as to the number or frequency of business suspensions, each suspension MUST NOT exceed one year. For example, if a business has been operating without a business plan for a long time but does not wish to disband, it must notify the business registration office.

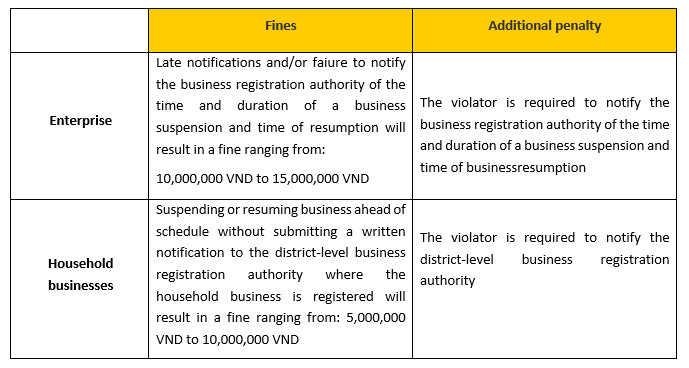

4. Penalties

The above is information pertains to the procedures for a company business suspension. For assistance in completing a procedure or to clarify the procedures, you may contact our team of legal experts via phone number +84-916-545-618 or email hung.le@cnccounsel.com and thanh.tran@cnccounsel.com for further assistance.